A new federal tax incentive is poised to have a large impact on District-supported real estate projects. Per last year’s federal tax overhaul, investments in real estate or businesses located in Opportunity Zones—low-income census tracts designated by states—can receive large capital gains tax breaks. The incentive is designed to drive investment to neighborhoods where private capital would otherwise be hesitant to invest. Yet DC’s chosen Opportunity Zones overlap substantially with the location of major District-supported real estate projects already underway, as well as areas that already have high levels of private investment. This points to a need for District policymakers to consider the value of all incentives available to investors when approaching real estate deals and adjust the level of District subsidy accordingly. The District should also more closely target incentives to areas where private investment is not already occurring.

Opportunity Zones offer significant tax benefits to investors. Capital gains taxes on investments in real estate and certain other assets located in Opportunity Zones (via an investment vehicle called an Opportunity Fund) can be forgiven if the investment is held for at least ten years; there are also tax discounts available after five and seven years. Moreover, investors can roll their other investments into an Opportunity Fund, defer the capital gains on that investment, and receive the same tax benefits as above.

There are many important policy questions surrounding Opportunity Zones. Because the tax benefits grow with the appreciation of the investments (e.g. rising property values) some experts worry that Opportunity Zones will serve as a subsidy for gentrification—especially because there is no requirement that investments provide any benefits for the community, such as affordable housing or high-quality jobs. Furthermore, place-based tax incentives have a poor record of success in attracting new investments that would not have occurred otherwise. Finally, the underlying premise of Opportunity Zones—that funneling capital investment into poor neighborhoods will, in and of itself, create new economic opportunities for low-income residents—is questionable.

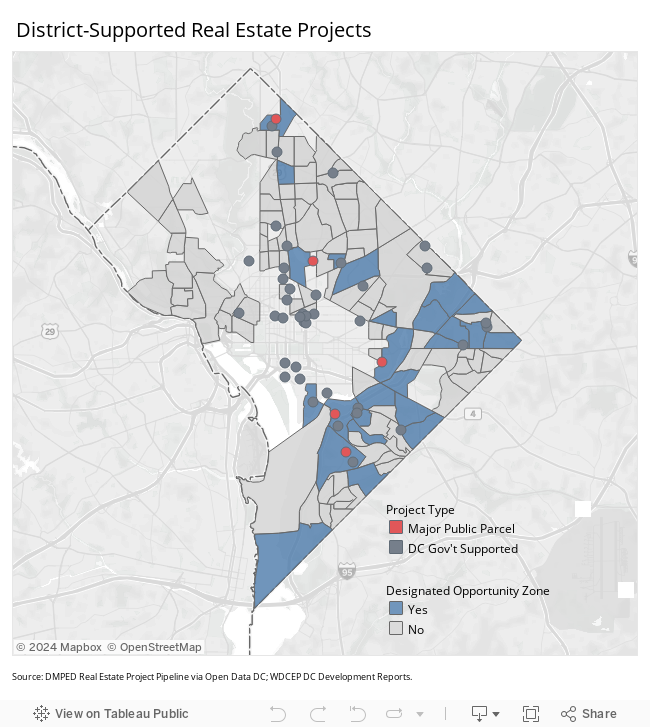

An examination of the District’s designated[1] Opportunity Zones reveals yet another concern: substantial overlap of the chosen tracts with the city’s pipeline of real estate projects—including every eligible major publicly owned land parcel slated for redevelopment. This means additional unplanned-for benefits for investors in developments that are already happening:

- Large public parcels: Walter Reed, Reservation 13 (Hill East), Poplar Point, and Saint Elizabeths.[2]

- City-supported real estate development projects: including Buzzard Point (DC United Soccer Stadium), Skyland Town Center, and the Bryant Street TIF.

The District may have intended to give a special boost to developments it is already supporting.[3] However, unless the full package of District subsidies—such as land discounts, tax abatements, grants, infrastructure financing, and other place-based incentives— is reduced to account for the value of Opportunity Zone tax breaks, the District will have enabled investors to “double dip”: to receive several layers of incentives without providing a commensurate level of public benefits.[4]

Unfortunately, subsidy packages for many of the real estate developments now covered by Opportunity Zones have already been approved. This points to a need for the District to be transparent going forward about the value of every incentive or subsidy—federal or local—available to a development project.

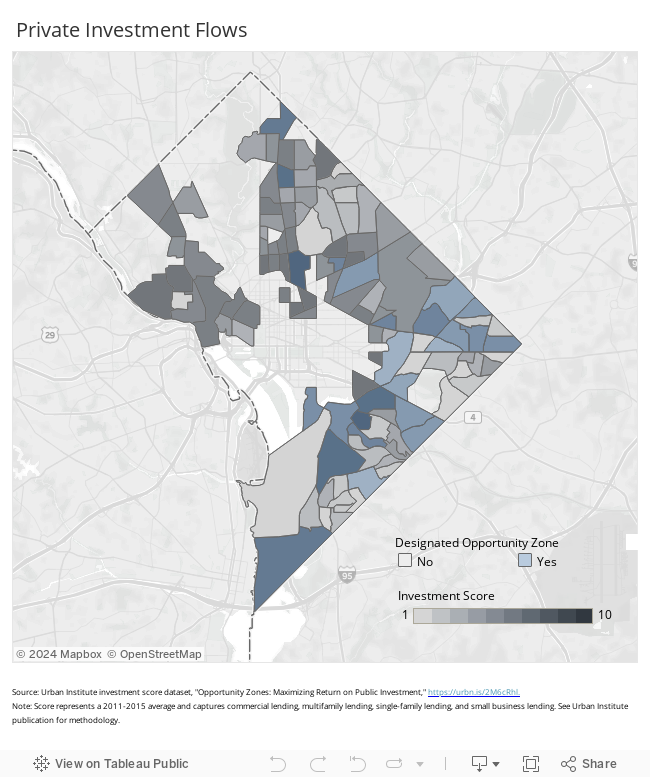

Finally, many of DC’s Opportunity Zones already have high levels of private investment. According to an index developed by the Urban Institute that captures commercial lending, multifamily lending, single-family lending, and small business lending between 2011 and 2015, 20 percent of designated DC Opportunity Zone tracts have private investment flows above the 70th percentile among eligible DC tracts. Nearly all large public parcels designated Opportunity Zones have or are adjacent to areas with high levels of investment. Notably, the census tracts corresponding to Anacostia and Congress Heights show high private investment flows and are designated Opportunity Zones—while tracts with little current investment (such as the Douglass-Shipley Terrace area) have not received an Opportunity Zone designation.

This means that some areas with little pre-existing investment flow will receive no incentive benefit, while investors in several neighborhoods already on the verge of change will gain large tax breaks. In the latter, the mix of pre-existing investor interest and new incentives could be a precursor to accelerated gentrification—making it all the more important that the District adopt equitable development strategies and avoid missing opportunities to target incentives where investment is not already occurring.