DC can raise needed revenue and address tax inequity by taxing more of the gains, or proceeds, generated by wealth—such as capital gains, dividends, and other forms of passive income. DC’s tax system protects and grows wealth concentration through myriad preferences and loopholes, exacerbating racial and economic inequality. This special treatment also prevents the District from generating the revenue needed to adequately fund programs and services. Applying a tax on proceeds generated from wealth is a simple way for DC to raise hundreds of millions of dollars to help struggling residents withstand the local recession and drastic federal and local safety net cuts.

DC Can Raise Revenue and Improve Equity with a Wealth Proceeds Tax

DC can levy an additional local percentage (or a surcharge) to the federal Net Investment Income Tax (NIIT), as recommended by the Institute on Taxation and Economic Policy (ITEP).[1] Federal lawmakers adopted the NIIT to support implementation of the Affordable Care Act, asking people with passive income, largely from capital gains (e.g., from cashed-in stocks), to pay a 3.8 percent tax on wealth that exceeds a relatively high threshold. The NIIT applies only to wealth that exceeds a modified adjusted gross income of $200,000 for single filers and $250,000 for married filers.[2] For example, a resident with $150,000 in wage income and $75,000 in capital gains would owe NIIT on just $25,000 of their capital gains.

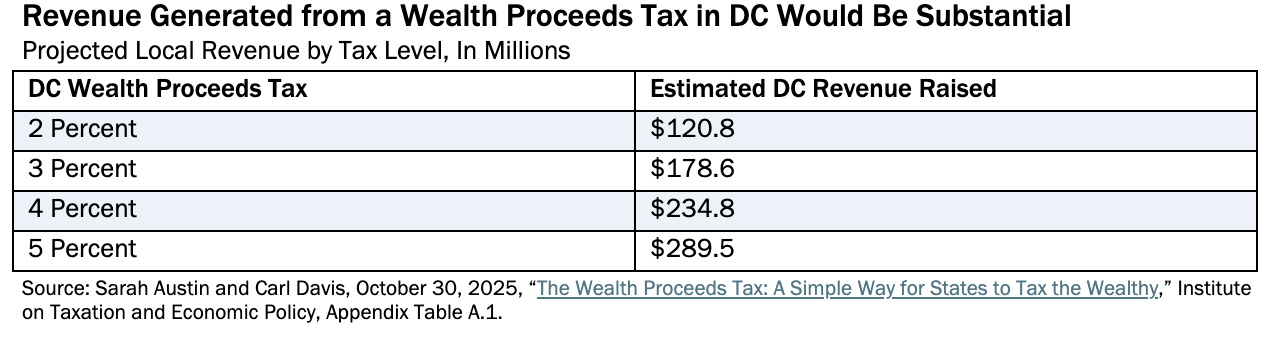

DC could simply add a local tax of 2 percent, or higher, to that same wealth reported to the federal government to yield substantial new annual revenue (Table 1).

TABLE 1.

In addition, a wealth proceeds tax would help DC recoup some of the massive tax breaks going to DC’s wealthiest households under the One Big Beautiful Bill Act (OBBBA).[3] Over 70 percent of the nearly $1.4 billion in federal tax cuts to the District went to families within the top 20 percent of incomes and 42 percent went to the top 5 percent alone, which are predominantly white families in DC.[4] Federal lawmakers paid for those tax cuts in part through severe cuts to health care, food assistance, and other critical programs DC residents rely on, all of which puts massive pressure on DC’s budget.[5] This coincided with mass federal layoffs that are reducing DC revenue and lawmakers’ ability to maintain local basic needs programs. A local wealth proceeds tax would help offset these losses and the increased tax inequity fueled by federal tax cuts.

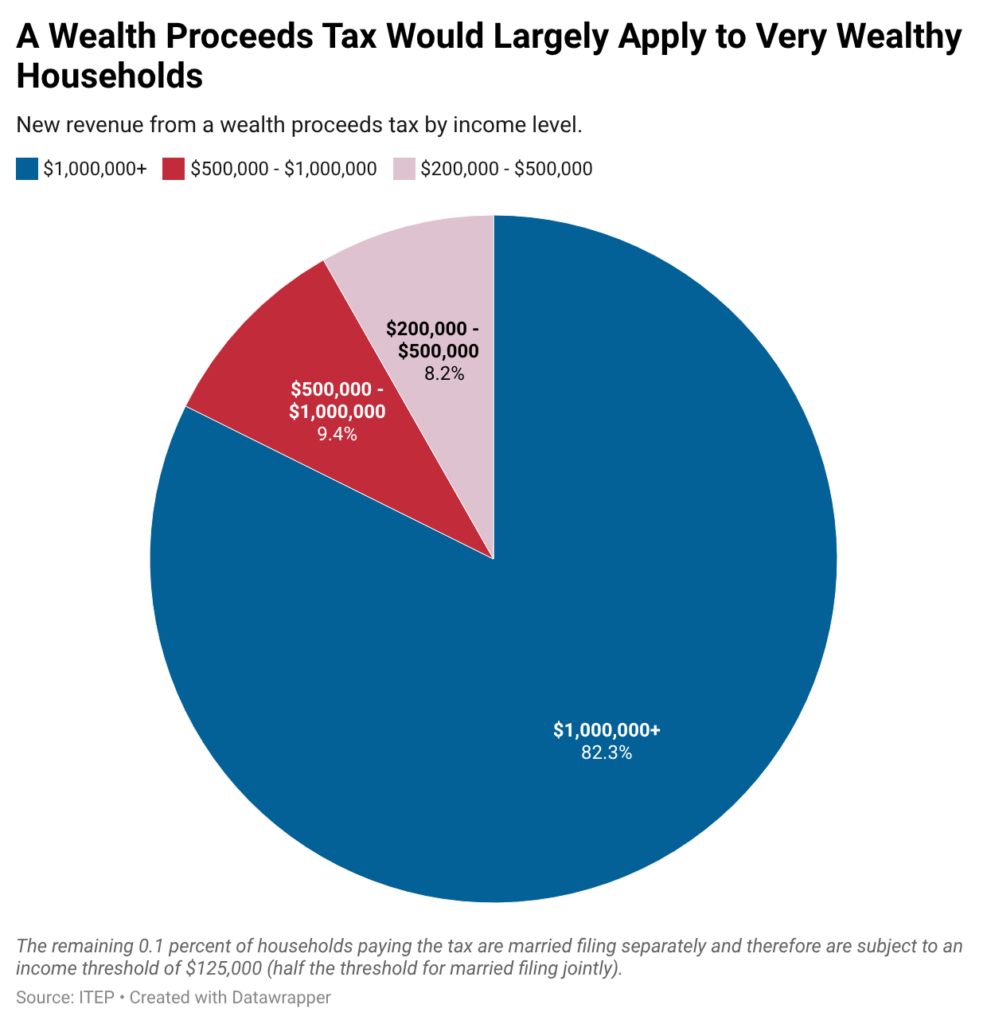

A Wealth Proceeds Tax Would Largely Apply to Very Wealthy, Predominantly White Households

Just 9 percent of DC taxpayers would pay the wealth proceeds tax, and it would largely fall on the very wealthy, according to ITEP. For example, about 82.3 percent of the new revenue would come from households with incomes over $1 million; another 9.4 percent would come from households with incomes between $500,000 and $1 million; just 8.2 percent would come from households between $200,000 and $500,000 (Figure 1). A history of racist policies that denied Black and non-Black people of color wealth-building opportunities has meant that high levels of wealth in DC and nationally continue to be predominantly held by white people. Nationally, 82 percent of stocks—which make up the lion’s share of capital gains—held by people with incomes above the NIIT thresholds are held by white people, while just 0.5 percent of those stocks are held by Black people and 0.5 percent are held by Hispanic people, according to ITEP.[6]

Below are examples of how a 2 percent wealth proceeds tax would work and who would and would not pay it:[7]

For those with small amounts of wealth, the tax would be very small…

Example 1: A married couple with joint earned income of $225,000 and realized capital gains of $40,000, or $265,000 in combined earned and passive income, would pay 2 percent on the $15,000 of their wealth that exceeds the $250,000 NIIT threshold. This couple would pay $300 in the DC wealth proceeds tax under a joint return.

For those with vast amounts of wealth, the tax would still be manageable relative to their income…

Example 2: A single person with earned income of $2,000,000, and another $1,500,000 in passive income derived from realized capital gains, would pay 2 percent of the $1,500,000 in wealth-derived income, or $30,000. That’s less than 1 percent of their total income.

For those with one-time inherited wealth, the tax may not apply…

Example 3: A married couple with $150,000 in income and $150,000 from the sales of newly inherited stocks from a deceased parent, which are sold before they appreciate, would not pay any tax on the $50,000 in gains that exceeds the $250,000 threshold. That’s because under current law, a person inheriting wealth does not pay on any of the gains accrued before they held the asset(s).

For those below the NIIT threshold, the tax does not apply at all…

Example 4: A single person has earned income of $75,000 and proceeds from the sale of an inherited home from a deceased parent of $300,000, with $175,000 of those proceeds reflecting gains accrued by the deceased parent and $125,000 reflecting gains accrued to them since inheriting the home. This person has a total income of $375,000 but still would not owe the wealth proceeds tax. That’s because, under current law, they would not owe tax on any gains accrued to the home while owned by their parent. In addition, the gains accrued under their ownership of the home ($125,000) before the sale plus their earned income ($75,000) do not exceed the $200,000 threshold.

A Wealth Proceeds Tax Would Be Simple to Administer

Taxing wealth through a tax on an already existing federal tax would also be simple to implement. DC can piggyback on federal tax filings simply by adding a local tax, which minimizes administrative costs for both taxpayers and the Office of Tax and Revenue. The federal government already defines what counts as wealth-derived passive income, so DC can simply adopt that framework. And DC would not be the first jurisdiction to do this. In 2023, Minnesota decided to piggyback on the federal NIIT, using a straightforward law to tax wealth.[8] The state is now generating substantial new revenue.

[1] Sarah Austin and Carl Davis, October 30, 2025, “The Wealth Proceeds Tax: A Simple Way for States to Tax the Wealthy,” Institute on Taxation and Economic Policy.

[2] “Questions and Answers on the Net Investment Income Tax,” Internal Revenue Service, webpage updated September 13, 2025.

[3] “Trump Tax Law: Research and Resources,” Institute on Taxation and Economic Policy, May 2, 2025. See the both the downloadable spreadsheet and graphic for the District of Columbia.

[4] Ibid.

[5] Erica Williams, May 16, 2025, “US House Details its Cruel Plan to Take Food and Health Care from the Poor to Give to the Rich,” DC Fiscal Policy Institute.

[6] Sarah Austin and Carl Davis, October 30, 2025, “The Wealth Proceeds Tax: A Simple Way for States to Tax the Wealthy,” Institute on Taxation and Economic Policy. See footnote 27.

[7] For additional examples of who the federal NIIT applies to, see: “Questions and Answers on the Net Investment Income Tax,” Internal Revenue Service, webpage updated September 13, 2025.

[8] 2024 Minnesota Statutes, Section 290.033, “Net Investment Income Tax,” accessed February 2026. In addition, other states may follow suit with bills in Hawaii, Virginia, Vermont, Indiana, Colorado, New Mexico, and New York.